GLP-1 Mono Agonists

The foundational class of obesity and diabetes drugs: one molecule, one receptor, two decades of iteration.

GLP-1 is the body's "enough" signal after a meal. A GLP-1 mono-agonist is the same signal, turned way up and held on for days at a time. Dozens of drugs sit in this class, and semaglutide alone has reshaped obesity medicine.

Counts reflect publicly disclosed programs in our database. Earlier-stage or undisclosed assets may not yet be represented. Approved count covers molecules currently on the US market; exenatide (Byetta / Bydureon, AstraZeneca, discontinued Oct 2024), albiglutide (Tanzeum, GSK, 2018), and lixisenatide (Adlyxin, Sanofi, 2023) are not counted.

Re-checked August 3, 2026

Every claim on this page is re-verified against sources including ClinicalTrials.gov, regulatory actions, press releases, and the published literature, all tracked in the GLP-1 Observer database.

GLP-1 mono-agonists are the drugs that made obesity pharmacology a serious therapeutic category. Semaglutide (sold as Ozempic for type 2 diabetes and Wegovy for obesity, each now in both injectable and daily-pill forms) turned a modest endocrine medicine into one of the largest drug franchises in the world and pulled the whole field along with it. Four of these drugs are currently on the US market. The most recent, orforglipron (branded Foundayo), joined in April 2026 as the first non-peptide GLP-1 pill ever approved, and more than 40 more are in development chasing longer dosing intervals, oral formulations, or lower prices. The class is also entering its generic era unevenly around the globe, with cheap semaglutide now available in India and other lower-cost markets and still years away in the US.

How GLP-1 mono agonists work

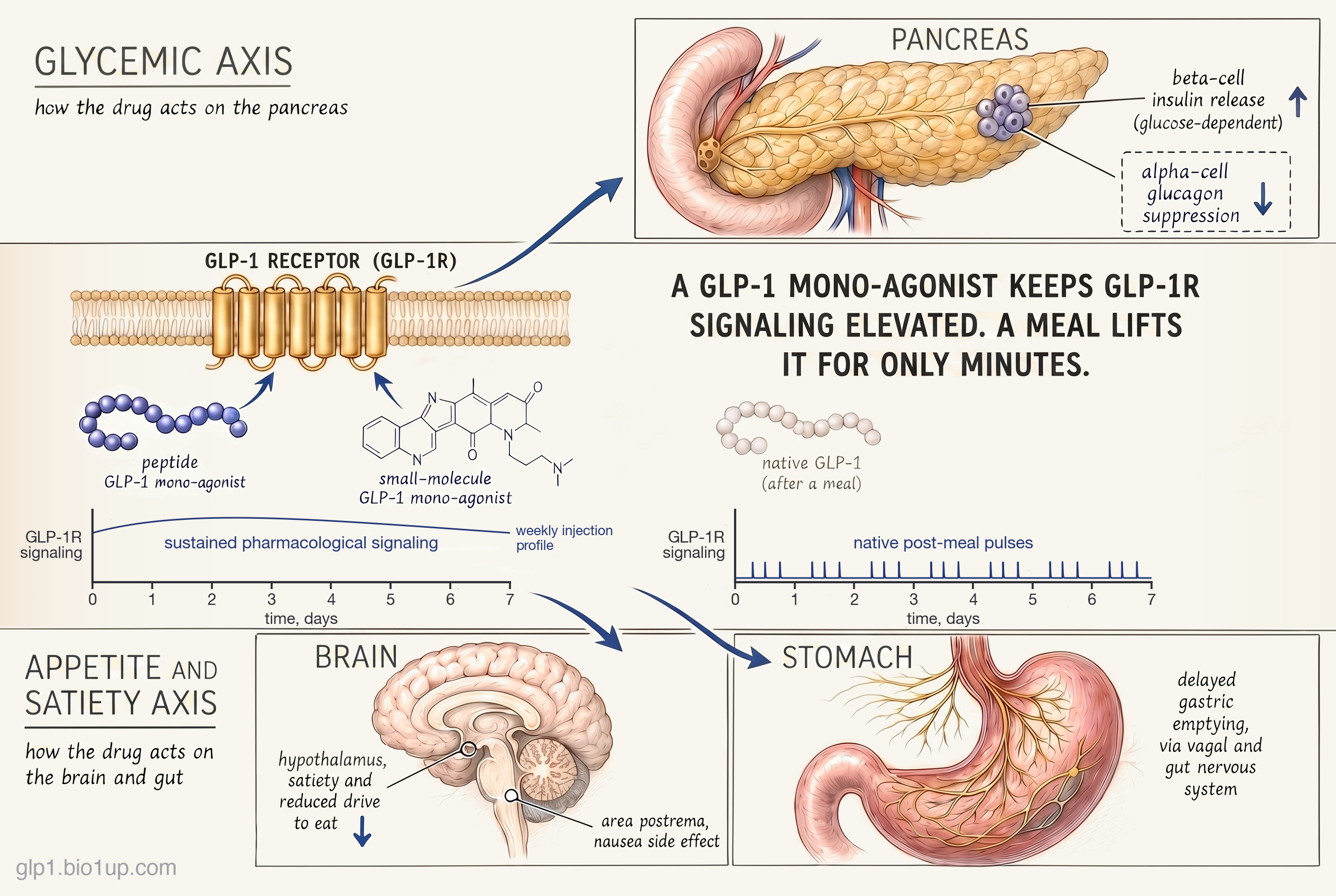

GLP-1 (glucagon-like peptide-1) is one of the body's gut hormones, released from specialized cells in the small intestine after a meal. Its native job is to tell the pancreas to release insulin in proportion to the glucose just absorbed (while suppressing glucagon, the sugar-raising hormone), to slow the rate at which food leaves the stomach, and to signal fullness to the brain. It is also short-lived: an enzyme called DPP-4 degrades it within minutes. So in a healthy person, GLP-1 rises sharply after a meal and falls back down almost as quickly.

A GLP-1 mono-agonist is a molecule that activates the same receptor that GLP-1 binds to, but at doses and durations the body never produces naturally. Where a meal triggers a transient GLP-1 pulse lasting minutes, a weekly injection of semaglutide keeps the receptor activated across the full seven days, even as drug levels rise to a peak and then gradually decline between doses. The dose matters too: a therapeutic injection delivers a pharmacological level of agonism, well above anything physiology ever generates. Sustained pharmacological activation of the GLP-1 receptor produces effects that meal-triggered pulses don't, and that is where the dramatic weight loss comes from.

The GLP-1 receptor is in more than one place. Activating it on pancreatic beta cells drives the glucose-dependent insulin release that makes these drugs useful in type 2 diabetes. Activating it on the gut's nervous system (vagal afferents and enteric neurons) delays gastric emptying, which contributes to the feeling of fullness after a meal. But the biggest contribution to weight loss comes from the brain. Receptors in the hypothalamus (where the body integrates satiety signals) and in reward-processing regions reduce the drive to eat beyond the simple sensation of being full. Receptors in the area postrema, a part of the brainstem that triggers vomiting, are a primary reason nausea is the most common side effect.

The same molecule produces different clinical pictures depending on the dose. At the lower doses used for type 2 diabetes (semaglutide 0.5 to 2 mg weekly), glycemic improvement is the dominant effect and weight loss is modest. At obesity doses (semaglutide 2.4 mg weekly, or 25 mg in the daily oral form), appetite reduction dominates and average weight loss in pivotal trials reaches about 17% of baseline body weight in patients who stay on the drug (real-world averages, which include the effect of patients who stop, run a few percentage points lower). A higher-dose injectable (semaglutide 7.2 mg weekly, approved March 2026 as Wegovy HD) pushes this average to roughly 21%. Dual agonists like tirzepatide and triple agonists like retatrutide push higher still by adding other receptors to the mix, but the GLP-1 mono class remains the foundation against which every other incretin-based obesity drug is measured.

The class has matured around this one receptor, but the molecules keep evolving. Where they are going next is below.

Where the class is evolving

The GLP-1 receptor is a single target, but the class keeps finding new room to move. Five developments stand out in the current pipeline and market.

Two approaches to the oral GLP-1

For most of the class's history, GLP-1 drugs had to be injected. The peptide doesn't survive a stomach full of acid and enzymes, and isn't absorbed well through the gut wall even when it does. Over a four-month stretch in late 2025 and early 2026, two drugs cracked the problem of oral weight-management GLP-1 dosing from different directions.

The oral form of Wegovy is the same semaglutide peptide as the Ozempic and Wegovy injections, packaged as a pill. To survive the stomach, each tablet co-formulates semaglutide with SNAC, an absorption enhancer that briefly raises the pH around the tablet and opens a short window of permeability through the stomach lining (the SNAC chemistry produces transcellular absorption specifically across the stomach epithelium).

Only about 1% of the dose reaches the bloodstream, so the tablet carries about 100x the injectable dose. This is the same technology Novo introduced with Rybelsus (oral semaglutide for diabetes) in 2019, now scaled to the 25 mg obesity dose.

Foundayo is not a peptide. It's a small molecule, built from scratch to bind the GLP-1 receptor. Because it isn't a peptide, stomach acid and gut enzymes don't degrade it, and its size and chemistry let it absorb through the gut wall on its own.

Because the molecule absorbs on its own, no absorption enhancer or dose multiplier is needed. Foundayo is the first non-peptide GLP-1 RA ever approved, and the first GLP-1 drug to take like a regular daily pill.

Both drugs are on the US market and directly competing. Several other non-peptide oral GLP-1 small molecules (Structure Therapeutics' aleniglipron among them) are advancing through clinical trials behind Foundayo.

Dosing interval and duration of action

The first GLP-1 drug, exenatide, had to be injected twice a day. The native GLP-1 peptide is cleared from the bloodstream within minutes, and exenatide's half-life was only about 2.4 hours. Every subsequent drug in this class has been, in one way or another, an engineering exercise in extending the half-life so patients can inject less often.

Three techniques have done most of the work. Fatty-acid attachment anchors the peptide to albumin in the bloodstream so the kidneys don't clear it as quickly; this is how liraglutide (daily) and semaglutide (weekly) each get their long half-lives, with semaglutide's longer fatty chain buying the extra days. A technology known as Fc fusion glues the GLP-1 peptide to an antibody fragment, and is how dulaglutide reaches a weekly interval. Microsphere depots encapsulate the peptide in slowly-degrading polymer beads so the injected dose releases over a week; this was the approach behind Bydureon, the first weekly GLP-1 injection, which AstraZeneca discontinued in 2024.

The trajectory has bent steadily toward less-frequent dosing. Twice-daily to once-daily to once-weekly. Investigational programs aim for once-monthly injectables, though none have been approved yet. Oral GLP-1s are the exception to the trend: their dosing is set by absorption constraints (for peptide pills) or by shorter molecular half-lives (for non-peptide small molecules).

At the far edge of the frontier, PegBio's CR059 is an early-stage circular-RNA therapy: the patient receives genetic instructions that tell their own cells to produce exenatide, not the peptide itself, potentially allowing dosing once a month or less often.

Tolerability and the titration curve

GI side effects define the GLP-1 experience, and the GLP-1 monos are the reference point against which every other class is measured. Nausea, vomiting, constipation, and diarrhea are the most common, and they're dose-dependent. Most patients feel them most sharply during the first weeks of a dose step-up, then the symptoms moderate.

The standard mitigation is titration: start at a dose too low to cause meaningful symptoms, step up every four weeks or so, and take 16 to 20 weeks to reach the full therapeutic dose. This is why GLP-1 drugs can't be started at the target dose the way many pills can. The titration curve also explains why real-world tolerability data often looks worse than clinical trial data: in trials, titration is enforced by protocol, but in clinical practice, patients and prescribers sometimes skip steps.

Newer molecules are being watched for whether they shift the tolerability profile. Foundayo's early data shows GI side effects broadly similar to injectable GLP-1s at comparable exposure levels, though the FDA has requested a post-marketing study on cardiovascular and liver safety signals from its obesity indication. Whether small-molecule pharmacology produces a meaningfully different side effect profile from peptides will take years of real-world data to settle.

The beginning of the generic era

For most of the class's history, every GLP-1 drug on the market has been patent-protected and branded. That began to change in late 2025 and early 2026, but unevenly, and along a geographic split that produces two very different pictures depending on where a patient lives.

The first GLP-1 generics reached the US market in late 2025 and early 2026, but only for liraglutide (Saxenda / Victoza). Teva, Cipla, and Biocon are all now marketing generic liraglutide.

Semaglutide is a different story. Novo Nordisk's patent thicket, combined with biosimilar exclusivity rules, blocks competing versions from the US market until around December 2031. Apotex has tentative FDA approval but cannot launch.

In India, Novo Nordisk's composition-of-matter patent on semaglutide expired in March 2026. In Canada the patent had already lapsed back in 2019, and a separate regulatory data-exclusivity period ended in January 2026, clearing the way for generics. Neither country requires the biosimilar pathway that gates entry in the US and EU.

More than 40 Indian generic semaglutide products launched within weeks at monthly prices around $15. Canada became the first G7 country to approve generic semaglutide. The first approvals (Dr. Reddy's and Apotex, spring 2026) were generic Ozempic, licensed for type 2 diabetes, and reached pharmacy shelves in May, though Dr. Reddy's has paused shipments over an ingredient quality issue it does not expect to resolve until late in the year. Apotex's Sevmia became the first generic cleared for chronic weight management in late June, and further approvals have followed. A similar pattern is expected in Turkey and South Africa as patents lapse.

The EU sits closer to the US side of this divide: supplementary protection certificates extend Novo's protection there into the early 2030s. China is a revealing in-between case: its semaglutide patent expired in March 2026, but a separate data-protection term tied to the China-Switzerland trade agreement keeps generics off the market until 2027, so Novo still has the market to itself there for now. Brazil is a distinct case: rather than a generic, its regulator approved a domestically made synthetic semaglutide (EMS's Ozivy) in May 2026 as a new drug, cleared for type 2 diabetes. The net effect is the start of a global split: cheap generic semaglutide is already widespread in India and has reached Canada, with more markets expected to follow as protections lapse, while the drug stays a premium-priced brand inside the biggest markets. The New York Times covered this split in detail in March 2026.

Beyond weight loss: cardiovascular, kidney, liver, and neuroscience

For most of the class's history, GLP-1 mono-agonists have been evaluated on the metabolic endpoints they were originally built for: glucose, body weight, and the quality-of-life measures that follow from those. Starting in the early 2020s, the scientific conversation has widened. The GLP-1 receptor is expressed well beyond the pancreas and the hypothalamus, and the clinical effects of chronic GLP-1 activation reach further than metabolism alone.

The most established extension is cardiovascular and kidney protection. The SELECT trial, reported in 2023, randomized more than 17,000 people with obesity and established cardiovascular disease but without diabetes, and showed that semaglutide reduced major adverse cardiovascular events by about 20% compared to placebo. The effect was larger than body-weight change alone would predict from prior weight-loss epidemiology, which suggests the cardiovascular benefits involve mechanisms beyond weight reduction, such as direct vascular effects or systemic anti-inflammatory action. The FLOW trial, reported in 2024, stopped early for efficacy and showed roughly a 24% reduction in a composite kidney outcome in people with type 2 diabetes and chronic kidney disease. The SOUL trial, reported in early 2025, extended the cardiovascular benefit to oral semaglutide in patients with type 2 diabetes plus cardiovascular or kidney disease. These trials have reshaped how the class is regulated. Ozempic carried a cardiovascular risk-reduction indication for type 2 diabetes plus established cardiovascular disease (CVD) from 2020 (on the strength of SUSTAIN-6); Wegovy gained a parallel CV indication in March 2024 for obesity plus established CVD regardless of diabetes (SELECT); semaglutide added a chronic kidney disease indication in January 2025 (FLOW); and Rybelsus gained a CV indication later in 2025 for type 2 diabetes plus CV or kidney disease (SOUL), on top of the class's original metabolic indications. In August 2025, the FDA further approved semaglutide for metabolic dysfunction-associated steatohepatitis (MASH, formerly NASH) based on the ESSENCE Phase 3 trial, extending the class into liver disease as well.

The newer frontier is the central nervous system. GLP-1 receptors are expressed broadly in the brain: in reward circuitry (the nucleus accumbens and ventral tegmental area) and in regions implicated in neurodegenerative disease. This breadth motivates two different lines of investigation: substance-use trials in alcohol, opioid, and nicotine dependence, and neurodegeneration trials in Parkinson's and Alzheimer's. The picture is mixed: early Phase 2 work in alcohol use disorder has shown modest reductions in craving and consumption, while the Parkinson's (Exenatide-PD3) and Alzheimer's (EVOKE) programs have read out negative. No GLP-1 mono-agonist has yet produced a regulatory approval in any neuroscience indication, and whether any of the investigational uses clears an approval bar is still open. But the pattern so far is that the GLP-1 receptor keeps proving more broadly implicated in human physiology than its first thirty years of drug development suggested, and the class will likely continue to be tested in new organ systems for years.

The competitive landscape

Landscape as of July 2026GLP-1 mono-agonists are commercially the most dominant drug class in modern pharma, and also the most lopsided. Four molecules are approved and on the US market, but semaglutide alone accounts for the overwhelming majority of prescriptions and revenue.

Novo Nordisk's semaglutide franchise (Ozempic for type 2 diabetes, Wegovy for obesity, and the newer oral forms of both) dwarfs every other drug in the class. It has helped make Novo one of the most valuable companies in Europe. Dulaglutide and liraglutide, the two long-established competitors, have been contracting sharply as prescribers and patients shift to semaglutide and tirzepatide: Eli Lilly's dulaglutide (Trulicity) has fallen from a 2023 peak near $7 billion to about $5.2 billion in 2024, with another steep drop in 2025 as Lilly's own tirzepatide cannibalizes it. Novo's Victoza, the type 2 diabetes brand of liraglutide launched back in 2010, has collapsed from about $3.7 billion at its 2018 peak to roughly $860 million in 2024 (its obesity sibling Saxenda still earns around $1 billion), and the first US generic liraglutide products arrived in 2025 to pressure it further. Orforglipron (Foundayo), the fourth and newest approved molecule, is the opposite story so far. It's growing, not shrinking. Exenatide, the very first drug in the class, is no longer on the US market; AstraZeneca discontinued it entirely in October 2024 as demand dried up. For practical purposes, the US mono-agonist market today runs on semaglutide, with a large fading tail of dulaglutide and liraglutide and a small new shoot called Foundayo.

Outside the approved set, the pipeline is broad and concentrated in a few places. Eli Lilly's orforglipron (Foundayo) just joined the market in April 2026 as the first non-peptide GLP-1 approved, and two more oral non-peptides are chasing it: Structure Therapeutics' aleniglipron (Phase 3) and AstraZeneca's elecoglipron, which has begun Phase 3 and marks the company's return to the class it left when it discontinued exenatide in 2024. Chinese biotechs have produced the deepest late-stage pipeline in the class: Huadong Pharmaceutical is running Phase 3 trials for two assets (HDM1002, an oral small molecule, and HDM1702, an injectable semaglutide biosimilar), Hangzhou Sciwind's ecnoglutide was approved in China for type 2 diabetes in January 2026 and for chronic weight management in March 2026 (Pfizer holds the China commercialization rights), and Hengrui and Gan & Lee each have Phase 3 obesity programs. Pfizer is running a Phase 3 injectable program (berobenatide, formerly MET-097i) acquired through its 2025 Metsera purchase, with a preclinical oral GLP-1 mono (MET-224) also in the pipeline.

For new programs, the commercial bar keeps shifting upward. A decade ago, matching semaglutide's efficacy was a sufficient goal. Now, new injectable GLP-1 monos have to compete with oral non-peptide options and with the even-higher-efficacy dual and triple agonist classes. The race to watch over the next 12 to 18 months: whether any of the late-stage challengers differentiate on tolerability, formulation convenience, or price enough to pull meaningful share from semaglutide, or whether the next real gains for obesity treatment come entirely from the dual and triple classes.

Drugs in this class

| Drug | Developer | Formulation | Stage | Conditions |

|---|---|---|---|---|

| Semaglutide | Novo Nordisk | Weekly injection (Ozempic, Wegovy, Wegovy HD); daily oral (Ozempic pill, Wegovy pill) | Approved | Type 2 diabetes, obesity, cardiovascular risk |

| Liraglutide | Novo Nordisk | Daily injection; US generics from 2025 | Approved | Type 2 diabetes, obesity |

| Dulaglutide | Eli Lilly | Weekly injection | Approved | Type 2 diabetes |

| Orforglipron (Foundayo) | Eli Lilly | Daily oral (non-peptide small molecule) | Approved Apr 2026 | Obesity |

| Aleniglipron (GSBR-1290) | Structure Therapeutics | Daily oral (non-peptide small molecule) | Phase 3 | Obesity |

| Elecoglipron (AZD5004) | AstraZeneca | Daily oral (non-peptide small molecule) | Phase 3 | Obesity, type 2 diabetes |

| Ecnoglutide (XW003) | Hangzhou Sciwind Biosciences (Pfizer China rights) | Weekly injection | Approved in China | Obesity, type 2 diabetes |

| HDM1002 | Huadong Pharmaceutical | Daily oral | Phase 3 | Obesity |

| HDM1702 | Huadong Pharmaceutical | Weekly injection | Phase 3 | Obesity |

| Berobenatide (MET-097i / PF-08653944) | Pfizer (via Metsera) | Monthly injection (extended-interval) | Phase 3 | Obesity |

Also in this class

- GZR18 · Gan & Lee · Phase 3 (obesity)

- HM11260C · Hanmi Pharmaceutical · Phase 3 (obesity)

- ASC30 · Ascletis · Phase 2 (obesity, both injection and oral)

- IBI3032 · Innovent · Phase 1 (obesity, oral)

Additional earlier-stage programs are running in multiple Chinese biotechs, and two semaglutide biosimilars are in development.

Withdrawn or discontinued

Three approved GLP-1 monos have been pulled from the US market in the past decade, all for commercial rather than safety reasons. Tanzeum (albiglutide, GSK) was withdrawn in 2018 when GSK decided to exit the class; weight loss and A1C reductions were modest compared with peers, and sales never reached a level that justified continued manufacturing. Adlyxin (lixisenatide, Sanofi) was withdrawn from the US in 2023 for similar reasons, though it remains available in some other markets. And Byetta and Bydureon (exenatide, originally Amylin Pharmaceuticals, later AstraZeneca) were discontinued in October 2024, ending the commercial life of the first drug in the class; AstraZeneca cited declining demand as prescribers and patients migrated to semaglutide and tirzepatide.

In a crowded class, being second or third best on efficacy has been enough to kill a drug commercially even when the safety profile was fine.

Related and adjacent mechanisms

Several related approaches sit close to this class. Some are variants of GLP-1 activation itself; others combine GLP-1 with additional receptor targets.

Bias the signal: biased GLP-1 agonists

Biased GLP-1 agonists are still GLP-1-only drugs, in the sense that they activate the same receptor as semaglutide and the others covered above. What differs is how they engage it. When GLP-1 binds its receptor, several different intracellular signaling pathways fire at once. The two most studied are cAMP (associated with the glucose-control and weight-loss effects) and beta-arrestin recruitment (associated with receptor desensitization over time and possibly with some of the GI side effects). A biased GLP-1 agonist is a molecule designed to preferentially trigger one pathway while minimizing the other, on the hypothesis that you can get the efficacy without some of the downstream costs. The idea has had a rough time in the clinic so far: Pfizer's danuglipron, once a lead oral biased GLP-1 program, was discontinued in April 2025 after a single potential liver-injury case in a dose-optimization study; an earlier Pfizer biased program, lotiglipron, had been pulled in mid-2023 for similar liver signals in Phase 1. But the underlying concept is alive and is already partly at work in approved drugs: tirzepatide (a GLP-1 / GIP dual agonist) is described in the literature as a biased agonist at the GLP-1 receptor (favoring cAMP signaling over beta-arrestin recruitment), though the clinical significance of that bias is still actively debated. A cleaner biased GLP-1 mono program could help re-validate the approach when it arrives.

Add a second receptor: GLP-1 / GIP duals and GLP-1 / amylin combinations

Adding a second receptor to the GLP-1 action is the most active area of obesity drug design today. Dual agonists pair GLP-1 with GIP (tirzepatide is the approved example; Viking's VK2735 and several Chinese programs are chasing in Phase 3) or with glucagon (Boehringer's survodutide and peers, aimed at larger weight loss with a metabolic-rate angle). Amylin combinations pair GLP-1 with cagrilintide (as in Novo's CagriSema) or activate both receptors from a single molecule (as in amycretin), pursuing the same goal through a distinct satiety pathway. Each of these approaches has its own field guide: GLP-1 / GIP duals, GLP-1 / glucagon duals, and GLP-1 / amylin combinations.

Add a third receptor: triple agonists

Triple agonists add a third receptor to the same molecule: GLP-1 plus GIP plus glucagon. Eli Lilly's retatrutide, the lead program, has produced the largest weight loss of any drug in trials so far: about 28% in its pivotal Phase 3 TRIUMPH-1 trial, which reported in May 2026. Novo Nordisk is advancing two tri-agonist programs of its own (one in-house, one licensed from a Chinese biotech), with Hanmi and others also in development. A dedicated field guide on triple agonists covers the details.

For how the GLP-1 mono drugs stack up beyond the mechanism, the GLP-1 Verdict grades them on efficacy and tolerability: see the scoreboard.

Frequently asked questions

What is a GLP-1 agonist?

A GLP-1 agonist is a drug that activates the GLP-1 receptor, the same receptor that a natural gut hormone called glucagon-like peptide-1 activates after meals. Activating this receptor reduces appetite, slows digestion, and prompts the pancreas to release insulin when blood sugar rises. The best-known GLP-1 agonists are semaglutide (sold as Ozempic for type 2 diabetes and Wegovy for obesity, in both injectable and daily-pill forms) and liraglutide (Victoza and Saxenda). They work by copying the natural signal at much higher doses and for far longer durations than the body ever produces on its own.

What's the difference between Ozempic and Wegovy?

Both are brand names for the same molecule, semaglutide: Ozempic is the type 2 diabetes brand and Wegovy is the obesity brand (at higher doses). Each now comes in two forms. Ozempic is a weekly injection and, in the US since 2026, a daily oral pill (this oral version replaced the older Rybelsus brand, which is still sold under that name outside the US). Wegovy is a weekly injection (including a higher-dose Wegovy HD at 7.2 mg weekly, approved March 2026) and a daily 25 mg oral pill for obesity (approved December 2025). The molecule is identical across all of them; what changes is the dose, the indication, and how it gets into the body.

Are oral GLP-1 drugs as effective as the injections?

Getting close, to varying degrees. Early oral GLP-1 options like Rybelsus (daily semaglutide for type 2 diabetes) produced less weight loss than the injectable versions, mostly because only about 1% of the dose was absorbed. The oral form of Wegovy at 25 mg daily produced around 17% weight loss in its pivotal trial, essentially matching injectable Wegovy at its 2.4 mg dose. Foundayo (orforglipron) showed roughly 12% weight loss in its pivotal Phase 3 obesity trial, which is meaningful but still several points below injectable Wegovy. (All figures here are efficacy estimates - weight loss in patients who stay on the drug; real-world numbers run a few percentage points lower.)

What are the side effects of GLP-1 drugs?

The most common side effects are gastrointestinal: nausea, vomiting, constipation, and diarrhea. They are dose-dependent and tend to peak during the first weeks of starting or stepping up a dose, then moderate. To limit them, GLP-1 drugs are titrated: started at a low dose and increased gradually over 16 to 20 weeks. Rare but serious warnings include pancreatitis, gallbladder problems, and a theoretical risk of medullary thyroid cancer (based on rodent studies; human relevance remains debated). Newer non-peptide drugs like Foundayo are being studied for whether their side-effect profiles differ from the peptide drugs that have dominated the class.

Are GLP-1 generics coming?

Yes, but unevenly. In the United States, the first GLP-1 generics arrived in late 2025 and early 2026 for liraglutide (Saxenda and Victoza), but semaglutide (Ozempic and Wegovy) is blocked from generic competition by patents and biosimilar exclusivity rules until approximately 2031. Outside the US, the picture is different. Novo Nordisk's composition-of-matter patent on semaglutide expired in India and China in March 2026. In Canada that patent had already lapsed back in 2019, with a separate regulatory data-exclusivity period ending in January 2026 and clearing the way for generics. Health Canada has since approved several generic semaglutides, first for type 2 diabetes and then, in late June 2026, for chronic weight management, with further approvals and submissions still following. More than 40 generic semaglutide products launched in India almost immediately, at monthly prices around $15. China is a partial exception: its patent expired too, but a data-protection term under the China-Switzerland trade agreement keeps generics off the market there until 2027. European protection extends into the early 2030s.

Recent newsletter coverage

Past pieces from the GLP-1 Observer newsletter that touched on this class.

- May 15, 2026 · Mechanism Explained: Beyond the Headline Number - "Early Responder" Segmentation: how Novo slices completed semaglutide trials by early-responder status to surface 21.6% and 27.7% headlines, and why that segmentation is becoming the competitive axis among the monos.

- May 1, 2026 · Mechanism Explained: What "Biased Agonism" Actually Means: the receptor-design strategy behind biased GLP-1 monos orforglipron, berobenatide (MET-097), and aleniglipron, and why partial and biased agonism widens the tolerability window.

- April 24, 2026 · Trial Spotlight: The Phase 3 Geographic Arms Race: five late-stage trials added roughly 500 clinical sites in a week, with the berobenatide (MET-097) and orforglipron outcomes trials showing that Phase 3 infrastructure has become the new moat in obesity.

References

- Drucker DJ. GLP-1-based therapies for diabetes, obesity and beyond. Nature Reviews Drug Discovery. 2025.

- Wilding JPH, et al. Once-Weekly Semaglutide in Adults with Overweight or Obesity. New England Journal of Medicine. 2021. (STEP 1 pivotal obesity trial)

- Pi-Sunyer X, et al. A Randomized, Controlled Trial of 3.0 mg of Liraglutide in Weight Management. New England Journal of Medicine. 2015. (SCALE pivotal obesity trial)

- Marso SP, et al. Semaglutide and Cardiovascular Outcomes in Patients with Type 2 Diabetes. New England Journal of Medicine. 2016. (SUSTAIN-6 cardiovascular outcomes)

- Buckley ST, et al. Transcellular stomach absorption of a derivatized glucagon-like peptide-1 receptor agonist. Science Translational Medicine. 2018. (SNAC absorption mechanism for oral semaglutide)

- Wharton S, et al. Orforglipron, an Oral Small-Molecule GLP-1 Receptor Agonist for Obesity Treatment. New England Journal of Medicine. 2025. (ATTAIN-1 pivotal obesity trial supporting Foundayo approval)

- Lincoff AM, et al. Semaglutide and Cardiovascular Outcomes in Obesity without Diabetes. New England Journal of Medicine. 2023. (SELECT cardiovascular outcomes trial)

- Perkovic V, et al. Effects of Semaglutide on Chronic Kidney Disease in Patients with Type 2 Diabetes. New England Journal of Medicine. 2024. (FLOW kidney outcomes trial)

- McGuire DK, et al. Oral Semaglutide and Cardiovascular Outcomes in High-Risk Type 2 Diabetes. New England Journal of Medicine. 2025. (SOUL cardiovascular outcomes trial for oral semaglutide)

- Sanyal AJ, et al. Phase 3 Trial of Semaglutide in Metabolic Dysfunction-Associated Steatohepatitis. New England Journal of Medicine. 2025. (ESSENCE Phase 3 MASH trial supporting August 2025 FDA approval)

- Hendershot CS, et al. Once-Weekly Semaglutide in Adults With Alcohol Use Disorder: A Randomized Clinical Trial. JAMA Psychiatry. 2025. (Phase 2 alcohol use disorder trial)

Track this class

GLP-1 Observer tracks clinical trials, news, and regulatory milestones across the GLP-1 and obesity-drug landscape, updated daily. See trial timelines, date-change alerts, and weekly roll-ups.